Private Sector Participation and Lead Logistics Partner Services – The key to unlocking the logistics deadlock in Southern Africa

While South African companies are searching for solutions in the face of a failing national carrier and the raining chaos in their supply chains, the private sector needs to accelerate their programme of private sector involvement in creating more effective logistics corridors.

Some movement has been apparent in the recent announcements of Transnet, namely privatising branch lines, accepting private sector rolling stock (wagons) on its network, integrating private security forces with its security on key export corridors, and spinning out of the Transnet port business as a separate entity.

The TFR Concessions Programme, which forms part of Transnet’s Private Sector Participation Plan (PSP), has been formally set out in the Transnet seven-year Corporate Plan. As announced by President Ramaphosa in early 2021, Transnet is embarking on a process of establishing concession opportunities with the support of and in consultation with the Government. The key here is for Transnet to fast-track these activities so that progress in throughput capacity, specifically for key mining commodities, can be demonstrated in the shortest period. Time is of the essence to save some of the mining houses from inevitable demise.

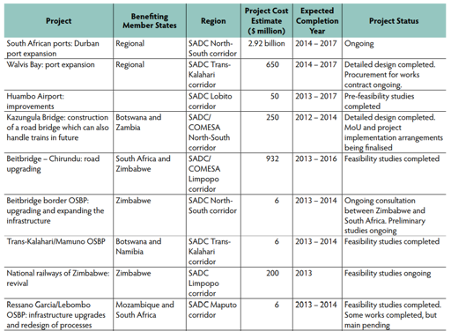

In 2012, the Southern African Development Community (‘SADC’) published a Regional Infrastructure Development Plan (RIDMP). Several wet and dry port projects were planned for construction or are currently in the early execution stages to facilitate several new or improved modal interfaces in the Transportation network. The rail link from Mchinji (Malawi) to Chipata (Zambia) would have a cargo terminal to serve the adjacent part of Zambia with rail access through Malawi to the Mozambican seaports. A dry port at Dona Ana and a container terminal at Tete (Mozambique) were planned to rehabilitate the Sena railway line to serve Malawi and eastern Zambia. Other dry ports were planned for Lusaka, Kitwe, and Edeola in Zambia, outside Dar-es-Salaam in Tanzania, at the Lebombo/Ressano Garcia border between South Africa and Mozambique and Walvis Bay in Namibia. The RIDMP at the time identified key transport projects for roads, railways, inland waterways, land borders, air, and seaports at the cost of 100 US$ billion over the fifteen-year plan period. The ambitious targets were unfortunately not achieved but should remain the focus of the SADC countries.

In the South African context, the development of appropriate logistics infrastructure has seen some significant drives towards improved dry ports, inland terminals, and intermodalism, seemingly following the world trend to containerise as much as possible. Containerisation is not always appropriate. The key enablers to reduce costs and improve performance in South Africa’s logistics industry are improved handling facilities for bulk materials in ports.

To this end, the Bigen Group has been instrumental in the planning, engineering, and project development of the Tambo Springs Intermodal Terminal and the Matsapha Container Terminal in Eswatini.

An extract of the planned project of the RIDMP is depicted below.

Table 1 -SADC Projects – Source RIDMP

Investment in rail, road, port, pipeline and airport infrastructure continues to be a high priority for the region, with hundreds of billions of dollars allocated annually in various projects, but no significant projects are ultimately completed. The ‘Swazi Rail Link’ is a case in point, and hence very little improvement in the throughput of goods or people can be demonstrated. Quite the contrary is occurring, but enough has been reported about this in recent times.

As is the case globally, funding for mega infrastructure projects is a significant constraining factor. Thus public-private partnerships (‘PPPs’) became the “go-to” solution for these projects to realise South Africa’s ambitious and infrastructure expansion plans. As described above, Transnet. in particular, is actively pursuing private sector engagement to drive forward its plans to promote infrastructure developments as it turned out that the very complex PPP structures initially offered to the market produced few tangible results.

Sustainability Challenges

The recent developments around ‘Mine/Pit to Port’ logistics in Africa have brought the real problems facing resource development in the region. Mining operations is an age-old activity with many mining houses successfully getting the desired form of their product ready for transportation to the off-taker at the mine gate. This is where the challenge starts in SADC. With all the best intentions in the world, the major rail SOE’s in Namibia, Zambia, DRC, Zimbabwe, and lately South Africa simply cannot cope with demands placed on the railway rolling stock and infrastructure.

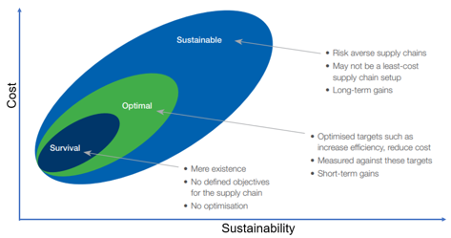

Having benefited of relatively intact infrastructure for decades, operators milked the system, withdrawing profits for other purposes. This resulted in crucial maintenance programs not being carried out, thus getting into the all too familiar situation of the ‘back of the drag curve’ conundrum: failing infrastructure with limited capital to upgrade or replace it.

Figure 1 – Maintenance spent on infrastructure and rolling stock – Source KPMG

Unmaintained rail infrastructure degrades slowly and silently, only emerging one day with a string of derailments and safety incidents starting to occur, resulting in cargo owners migrating their volumes to the road. Therefore, once the degradation has been detected, the reinstatement of this infrastructure is only possible with massive capital injections from the Development Finance Institutions (DFI’s). With further deterioration, rail enters a ‘death spiral’, becoming unfeasible, as railways become marginalised through the gradual, then sudden, freight movement from rail to road.

As the figure above illustrates, the cost for reinstatement of infrastructure and rolling stock balloons is beyond the ailing SOE’s capabilities. At this point, private sector participation becomes imperative, and the drive from railroads to allow private rolling stock on their infrastructure becomes non-negotiable.

The reasons for the movement from rail to the road are varied and many, but the most obvious reason is that over time, the rail service providers have become increasingly unreliable, a vicious cycle of aging equipment and infrastructure versus new and flexible road fleet competition.

Increasing rail tariffs to cope with the soaring maintenance and electricity prices costs does not help alleviate the problem.

Capacity Imperatives

A steady supply of transportation capacity to a mine in a steady state is not a luxury but a necessity. An imbalance between transportation capacity and product supply may put some of the largest miners at risk of going out of business fairly swiftly. A clear example of this is the recent reports of vessels off the south African coastline waiting weeks for product to become available on the berths with associated demurrage costs reaching into Billions. Swift changes from established ports of shipping to other more accessible points of export follow this debilitating trend. Supply chain optimisation companies called lead logistics partners or providers (‘LLP’) provide a valuable service to ensure that the cost for the shipper to get their product to a working port, onto a vessel, and to the customer is minimised.

The many billions of dollars touted by mining entrepreneurs in resource and mine development are often overshadowed by the development cost of the railway systems, deepwater ports, port stockyards, bulk material handling equipment, and transportation fleets to turn the resource into money.

Bigen Transportation has restructured its business to provide the three essential parts of moving products and minerals from Pit to Port or Factory to Port. These are:

- Bigen Transport Rail and Logistics to provide engineering solutions for rail infrastructure utilising the most reliable and cost-effective routes and ports from origin to destination;

- Bigen Transport Ports and Terminals providing engineering solutions for wet and dry port facilities with bulk materials handling systems; and

- 4th Party Logistics Services as LLP to its shippers, traders and 3rd Party Logistics service Provider customers.

The true cost of the infrastructure projects, including access to shared and new rail and port developments can be astronomical, so the team at Bigen supports asset owners with project development, feasibility studies, access to capital all the way to financial close. Understanding that the development of robust, economical transport infrastructure is a key driver to sovereign economic growth, Bigen aims at unlocking the value of undeveloped mineral resources in SADC.

Abundant mineral resources are of little value to the embattled Southern African countries unless brought to market at competitive rates. In a global context, Southern African countries understand the importance of such infrastructure development projects to make the SADC minerals internationally competitive. South Africa is well placed to capitalise on what many have described as the gateway for Southern Africa to International markets.

Market-driven developments in Supply Chain optimisation technologies

Recent developments in remote monitoring of logistics operations have spawned a surge in automation of the supply chain management industry. Remote Working Strategies (RWS) is the phrase coined to describe how modern mining, stockpile and logistics management, as contemplated by the likes of BHP and Rio Tinto, can now operate and control product flows from anywhere in the world.

These initiatives are extending beyond the mine gate with a significant commitment to driverless haul trucks, trains and other initiatives aimed at increased site safety by moving people out of harm’s way and replacing them with machinery.

With automation of operations comes the opportunity to track the consignment along the logistics chain in real-time – and so is born the true Pit to Port whole of logistics channel. This laser-focus on tracking allows the LLP to immediately deal with any disruption in the supply chain by implementing deviation management techniques, thereby ensuring the precious cargo reaches its end destination intact and on time.

Bigen Transportation is committed to developing supply chain management capabilities beyond the extent of mere stockpile management and weighbridge monitoring.

Mining houses of just a few decades ago characterised rail, road and port logistics chains as someone else’s problem. With the evolution of competitive logistics, miners need specialist companies to oversee how cargo arrives at the right speed and correct quantity at the port. This is, of course, an over generalisation in that larger miners very early understood the true impact of these networks on the viability and competitiveness of their product. They understood and sought to maximise the value of integration of mine, rail, materials handling, and ports across the entire logistics chain. In the recent past, the only true way to have such absolute integration was to own all of the elements – the mine, loading of trains, offloading at the port, and then ship loading in some cases.

Of course, this was not a viable option for the smaller miners, so it was very much a case of placing their trust in the carrier or, in other words, in the vagaries of someone else’s operations.

The Bigen LLP function

Identifying the optimal Pit to Port or Factory to Port solution in the case of bulk or containerised freight is critical to increase transportation asset productivity, eliminate double handling and modal wastage over the movement process of the product.

Bigen offers a full origin to destination service from loading and offloading site engineering to logistics monitoring systems. These services include preliminary and definitive feasibility studies, concept design and service design, project management and delivery, commissioning and logistics management. This service allows the mining house to concentrate on its core competency, namely low-cost mining.

The Bigen supply chain specialists analyse a range of feasible project solutions and select the solution that adds the most value to the project. Bigen have extensive knowledge in:

- Bulk material logistics & supply chain optimisation

- Simulation modelling

- Lifecycle cost analysis

- Regulatory risk and approval management

- Pit to Port route selection

- Best of breed equipment suppliers

- Construction estimating and procurement

- Construction management & Commissioning

- Bigen also has extensive experience in operations optimisation, which is focused on efficiency improvements, waste reduction and facility upgrade projects.

Bigen has helped mining and transportation companies create sustainable benefits by providing process optimisation and change management programs tailored to their specific requirements. As there is no standard “off the shelf” solutions for supply chains, Bigen analyses each unique situation and develops a custom approach to address the challenges and obstacles preventing a business from achieving its goals.

We believe that organizational development, behavioural change and coaching are key points to delivering improvements and ensuring the sustainability of benefits. Bigen’s approach is to transfer the necessary skills and continuous improvement methodologies to the client’s staff with the goal of creating sustainable value in the client’s business and “Doing good while doing business”.

Anton Willemse